Investing in Student Success:

Holding Universities Accountable for Student Loan Outcomes

Background

The U.S. federal government spends approximately $142 billion annually on higher education, including $89 billion in federal student loans.1 Despite the massive investment, outcomes for students and taxpayers are deeply troubling.

As of late 2025, undergraduate federal student loan default rates approached 25%, more than double the peak delinquency rate for single-family mortgages during the subprime housing crisis.2 These failures reflect poor economic returns: 23% of bachelor’s degrees and 43% of master’s degrees do not increase graduates’ earnings enough to justify their cost, leaving students with unsustainable debt and taxpayers with significant losses.3 Completion rates are also weak, with only 61.1% of students who entered postsecondary education in Fall 2019 earning a credential within six years.4

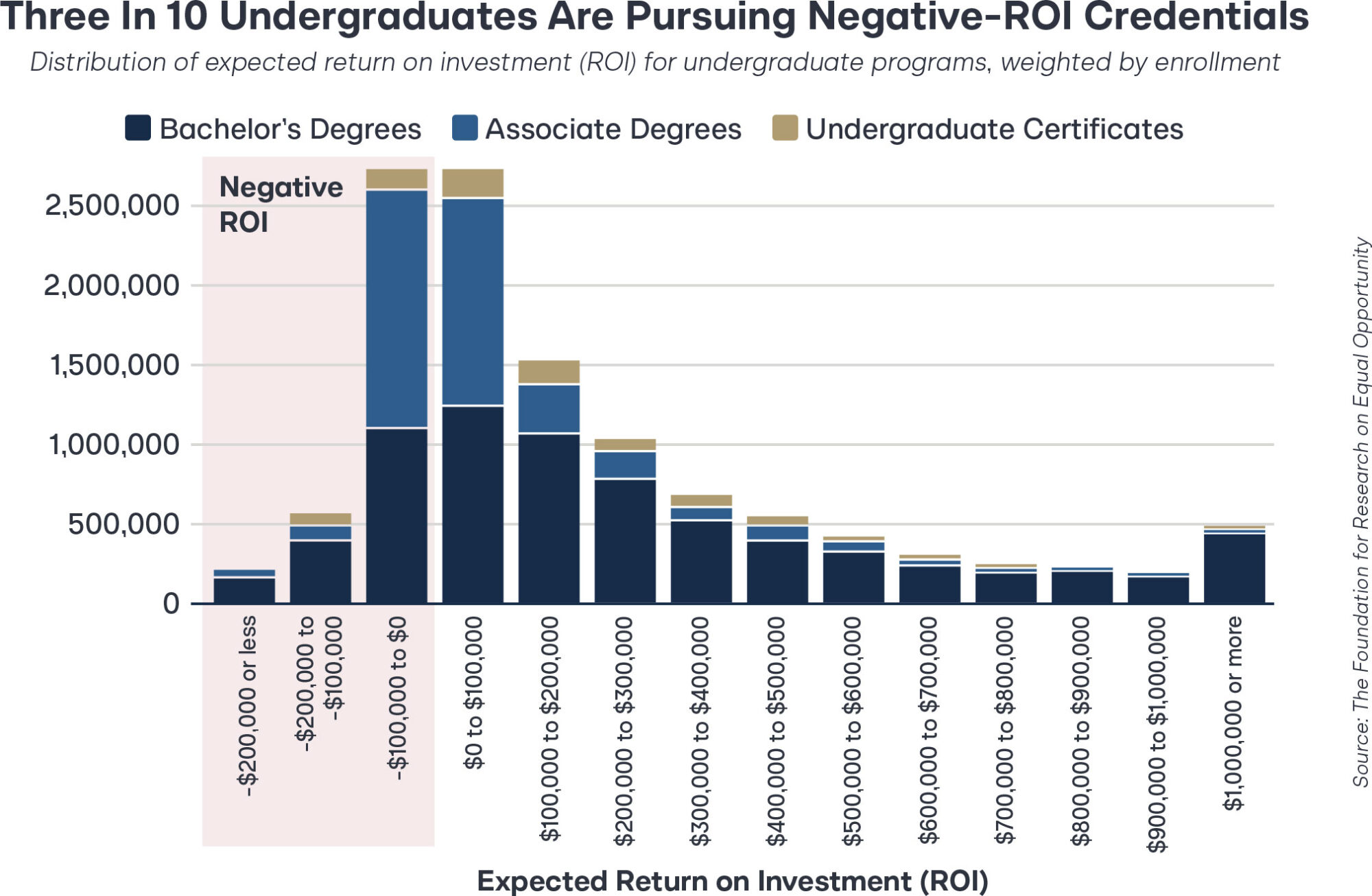

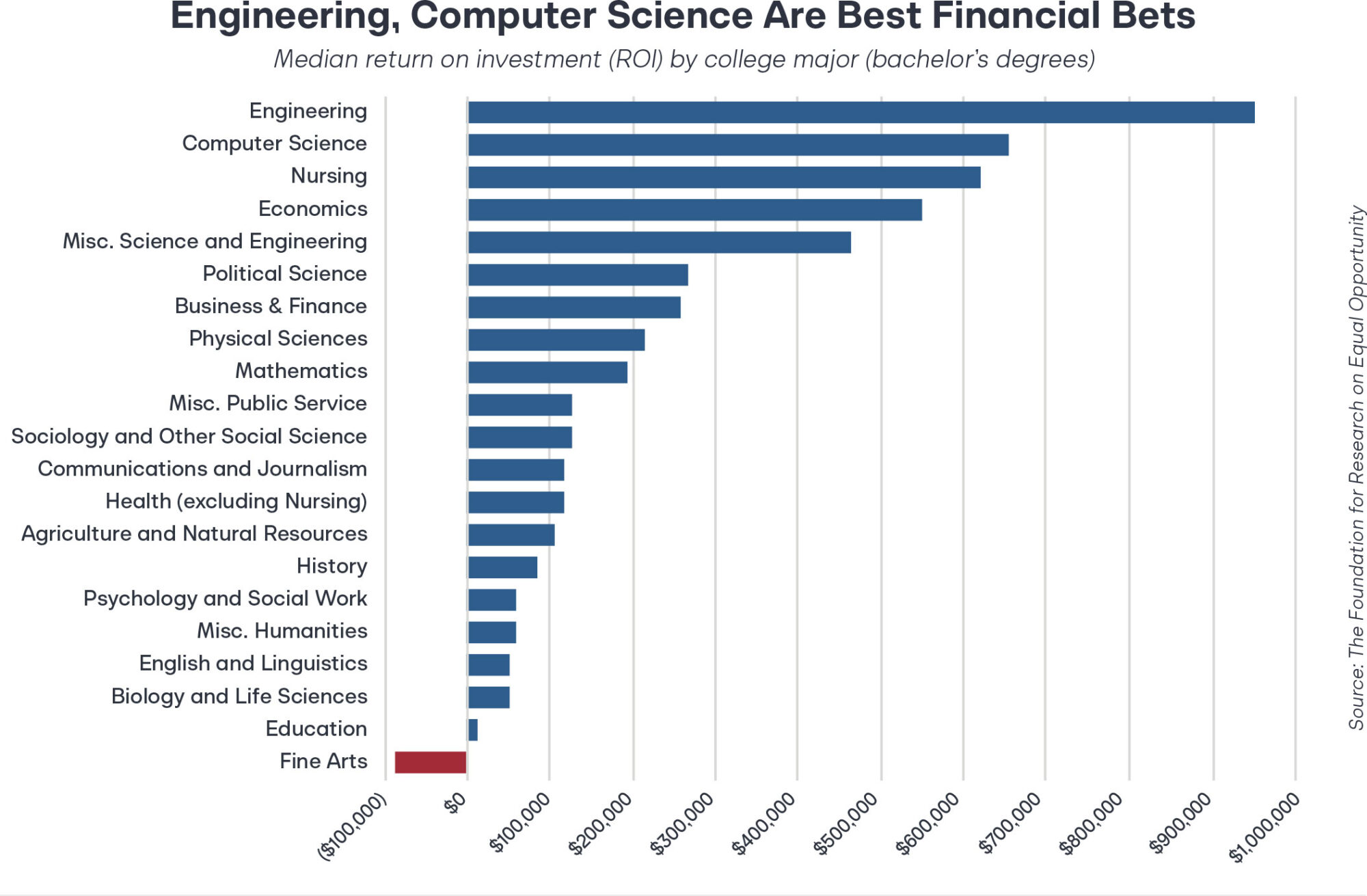

While median numbers make many majors appear to have a positive ROI for students, approximately 33% of students end up losing money on their college investment. To address this problem, accountability mechanisms indexed on schools and programs are critical, as the disparity between program and major performance by school is staggering.5

For example, at the University of Virginia, the business program’s ROI is over $3 million, while 13% of business programs nationwide have negative ROI. High tuition costs further exacerbate these failures. New York University, with an annual net cost exceeding $44,000, sees seven of its bachelor’s programs yield a negative ROI, including its film program at negative $22,000. Meanwhile, the same degree, a little upstate, at SUNY-New Paltz has a positive ROI of $148,000.6

The current system allows institutions to collect tuition upfront while students and taxpayers bear nearly all downside risk. This misalignment of incentives has produced predictable results and demands structural reform.

The Case for Institutional Accountability

To improve outcomes, colleges and universities must have meaningful financial responsibility for the loans their programs generate. Two existing policy pathways offer powerful tools to realign incentives without requiring new legislation.

- The College Cost Reduction Act (CCRA), introduced in 2024, would require institutions to reimburse the federal government for a portion of losses on defaulted or non-repaid student loans.7 While not enacted, the framework provides a strong blueprint for action.

- The Higher Education Act already grants the Department of Education broad authority to condition access to federal Direct Loans on program quality. Properly exercised, this authority could immediately cut off federal funding for programs that consistently fail to deliver value.

Why Program-Level Risk Sharing Matters

Risk sharing works best when applied at the program level, where outcomes are measurable and incentives are precise. Properly structured accountability avoids penalizing institutions that serve disadvantaged students while allowing low-return, high-cost programs to continue unchecked. When institutions are financially exposed to poor outcomes, programs that do not deliver economic value naturally contract or close, and capital is redirected toward programs that succeed. This is how incentives function in every other sector of a free market economy and higher education should not be exempt.

Existing Quality Assurance Authority Under Section 454 of the Higher Education Act8

Mandates that institutions participating in the federal Direct Loan program:

“[S]hall provide for the implementation of a quality assurance system, as established by the Secretary and developed in consultation with institutions of higher education, to ensure that the institution is complying with program requirements.”

This clause grants the Secretary of Education broad authority to define and enforce a quality assurance framework. To date, this authority has not been meaningfully used to incorporate outcomes into assessments of institutional quality.

Recommended Actions

The Department of Education should act on its existing authority under Section 454 (Deny Direct Loan Eligibility) to ensure that federal student loans support programs that deliver real economic value. The Department should also assess whether executive action or rulemaking could implement reforms inspired by and built upon the College Cost Reduction Act, including program-level risk sharing and loan guarantees.

- Deny Direct Loan Eligibility9

The most effective enforcement mechanism is to condition access to federal Direct Loans on measurable outcomes. Under a quality assurance framework established pursuant to Section 454, programs should be evaluated based on:

a. Debt-to-Earnings Test: Student loan debt must not exceed a defined share of a graduate’s annual earnings.

b. Earnings Premium Test: Undergraduate programs must produce earnings above those of a typical high school graduate, and graduate programs must exceed the earnings of a typical bachelor’s degree holder.

c. Default Rate Threshold: The current federal student loan program requires that a cohort’s default rate must not exceed 25% for three consecutive years or 40% in a single year. These thresholds are far too permissive and should be lowered.10

Programs that fail outcome standards in two out of three consecutive years should lose eligibility to enroll students using federal Direct Loans.

- Implement Risk Sharing11

The Department of Education should examine its rule-making authority to impose risk-sharing penalties on institutions whose programs fall below defined repayment benchmarks. Penalties should scale with the severity of repayment failure, ensuring that the worst-performing programs bear the greatest financial responsibility.

- Require Loan Guarantees12

The Department should also assess whether executive action can require institutions to financially guarantee a portion of the federal student loans taken out by their students. Under this model, universities would be required to purchase or post risk-based insurance on program-level student loans, with premiums tied to graduates’ repayment outcomes. Programs with strong labor-market returns would face low costs, while programs with weak outcomes would face higher premiums or become effectively uninsurable. This structure introduces a market-based evaluation of program quality, creates immediate incentives to improve outcomes, and ensures that institutions share responsibility when students cannot repay their loans.

Appendix

Stay Informed

Sign up to receive updates about our fight for policies at the state level that restore liberty through transparency and accountability in American governance.